Death benefit claims provide crucial financial support after losing a loved one by releasing superannuation balances and insurance coverage to eligible beneficiaries. However, navigating this process during grief can feel overwhelming. Unfamiliar paperwork and strict timelines only add to the challenge. This guide explains how these claims work in Australia. We cover who qualifies and what steps to take if complications arise. Our goal is to help you secure your full entitlements during an already difficult time.

What Is a Superannuation Death Benefit Claim?

A death benefit claim is the process of accessing the funds held in a deceased person’s superannuation account, including any life insurance attached to that account. Nevertheless, these funds aren’t treated the same way as assets in a Will. Instead, they’re governed by specific superannuation laws and the rules of the fund itself.

The death benefit usually includes:

- The total balance of the deceased’s super fund

- Any life insurance payout held within that fund

Death benefit claims are often a lifeline for loved ones who depended on the deceased’s income. But accessing this benefit can be legally complex, particularly if disputes arise or nominations are unclear.

Who Can Make a Death Benefit Claim?

Only certain individuals can legally receive super death benefits. Under Australian law, these people must fall into one of the following categories:

- Spouse or de facto partner (including same-sex partners)

- Children, regardless of age

- Financial dependants of the deceased

- Someone in an interdependency relationship with the deceased (where both parties provided financial and personal support)

- The deceased’s legal personal representative (usually the executor of the will or estate administrator)

If you do not meet one of these definitions, you generally cannot receive a death benefit directly from a super fund, even if you were close to the deceased.

How Death Benefits Are Paid: Understanding Nominations

The way a death benefit is distributed depends largely on whether the deceased made a valid beneficiary nomination. There are several types of nominations:

Binding Death Benefit Nominations (BDBNs)

This nomination requires the trustee to pay the death benefit exactly as instructed, provided it’s valid and up to date. There are two types:

- Lapsing BDBN: Expires after three years if not renewed

- Non-lapsing BDBN: Stays in place indefinitely (offered by some funds)

For a binding nomination to be effective, it must name eligible dependants and follow strict legal formatting.

Non-binding Nominations

These reflect the deceased’s preferences but are not enforceable. The trustee may consider these wishes alongside other factors—particularly if there are multiple eligible claimants.

Reversionary Beneficiary Nominations

This type of nomination applies to income stream accounts (like pensions). If valid, it allows the account to continue paying income to a beneficiary rather than being paid as a lump sum.

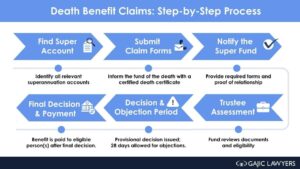

Step-by-Step Guide to Making a Death Benefit Claim

While each fund may have its own procedures, most death benefit claims follow a similar process:

- Identify all super funds the deceased had. There may be more than one.

- Contact each super fund and send them a certified copy of the death certificate to begin the claim.

- Complete and submit claim forms, with documents proving your eligibility (e.g. marriage certificate, financial records, etc.).

- Assessment phase – The trustee reviews the claim based on super laws and fund rules.

- Provisional decision issued – All potential claimants are notified.

- Claims staking period – Typically 28 days for objections to be made.

- Final payment – Once the dispute period has passed, the funds are distributed.

Some straightforward claims are resolved in a few months, but others—especially those involving disputes—can take much longer.

What Could Delay or Complicate a Death Benefit Claim?

Unfortunately, not all death benefit claims are simple. You may face roadblocks, especially if there’s no valid nomination or if multiple people believe they are entitled to the benefit.

Here’s a breakdown of the most common issues and how to handle them:

|

Issue |

What It Means | Recommended Action |

|

Multiple eligible claimants |

Several people are claiming the benefit | Seek legal guidance to strengthen your case |

| Expired or invalid nominations | Nomination wasn’t renewed or correctly signed | Regularly review and update nominations |

| Unclear dependency | Difficulty proving financial reliance | Provide thorough financial records |

| Objections from others | Another party disagrees with your claim |

Prepare for formal reviews or AFCA complaints |

| Lengthy delays by the fund | The process is dragging on unnecessarily |

Engage a Superannuation Lawyer for faster decisions |

Can I Dispute a Decision?

Yes. If the super fund decides to pay someone else or to distribute the funds in a way you believe is unfair, you can challenge that decision:

Step 1: Internal Review

If you disagree with the provisional outcome, you must submit your written objection within 28 days. The trustee will reconsider and may change their decision.

Step 2: AFCA Complaint

If you’re still not satisfied, you can lodge a complaint with the Australian Financial Complaints Authority (AFCA). AFCA is an independent body that can override a trustee’s decision if it finds it to be unfair, unreasonable, or inconsistent with the law.

Step 3: Court Action

This is typically a last resort. Legal proceedings in the Federal Court are only available for legal questions, not simply because you disagree with the outcome. These cases can be expensive and take years to resolve.

Are There Tax Implications?

Yes, and it’s crucial to understand how tax affects death benefit payments.

- Tax dependants (like spouses or minor children) usually receive payments tax-free

- Non-tax dependants (like adult children not financially dependent) may have to pay tax on the taxable portion of the benefit

- Income streams paid to beneficiaries may attract tax depending on their age and the deceased’s age at the time of death

If you’re unsure about the best approach, financial advice can help reduce tax so you can get the most from your benefit.

ASIC Report: Why the Process Needs Reform

In March 2025, the Australian Securities and Investments Commission (ASIC) released a comprehensive report revealing major shortcomings in how some super funds handle death benefit claims. The findings included:

- Claims taking longer than 500 days to finalise

- Lack of support for grieving families

- Poor communication and follow-up from trustees

The report made 34 recommendations, aimed at improving efficiency, fairness, and transparency in the handling of these critical claims. Some reforms are already underway, but progress varies across the industry.

Should You Get Legal Advice?

In many cases, yes. Legal advice is particularly important when:

- The trustee has made a decision you want to challenge

- Multiple people are claiming the benefit

- There’s no valid or clear nomination

- Your dependency status is likely to be contested

- You believe the process is unreasonably delayed

The earlier you speak with Gajic Lawyers, the more likely you are to avoid complications and secure your rightful benefit.

Planning Ahead: Protecting Your Loved Ones

You can reduce future complications by taking the following steps now:

- Make sure your super fund has a valid binding nomination in place to direct your benefit.

- Review lapsing nominations every three years

- Share your intentions with family members to prevent misunderstandings or disputes later.

- Your super doesn’t automatically go through your Will, so include it in your estate planning.

- Legal and financial guidance can give you peace of mind that your super will be handled as you intend.

Commonly Asked Questions About Death Benefit Claims

Q: How long will a death benefit claim take?

A: It depends on the complexity of the case. However, AFCA sees 3 months as a reasonable timeframe. In April 2025, AFCA reported that 94% of death benefit claims were finalised within 2 months, and 99% within 6 months.

Q: Can I see the documents submitted by someone objecting to the superannuation death benefit distribution?

A: Super funds generally won’t disclose the specific documents or amounts claimed by other parties due to privacy obligations. However, if you are an eligible claimant and an objection affects your potential share, the fund must give you enough information to understand the objection and respond. You can request a summary or ask what details they can legally share.

Q: How much can I expect to receive from a death benefit claim?

A: The amount depends on the super balance, any life insurance, and how the fund divides the benefit among eligible claimants. It varies case by case, and applies similarly across all Australian states. Call us now for expert advice.

Conclusion

Death benefit claims are a lifeline for many families navigating grief and financial uncertainty. But the process can be more complicated than people expect—especially if disputes arise or the super fund delays the claim. By understanding your rights, preparing properly, and seeking help when needed, you can take control and ensure your loved one’s legacy is protected.

Expert Legal Help for Grieving Families

At Gajic Lawyers, we understand that dealing with the legal side of losing someone is overwhelming. Rest assured, we will help you navigate the death benefit claims process with clarity, care, and expertise. We work with families across Australia to secure their rightful superannuation entitlements—whether you’re making a first-time claim, disputing a decision, or facing unreasonable delays. With years of experience handling complex superannuation and TPD claims, we’ll guide you every step of the way, ensuring your voice is heard and your rights are protected during this difficult time.

If you wish to start a death benefit claim or if you’re unsure where you stand, don’t hesitate to talk to one of our TPD Lawyers Sydney, Superannuation Lawyers Cabramatta, Car Accident Lawyers Perth, Superannuation Lawyers Adelaide, or Superannuation Claims (TPD) Lawyers Brisbane today.

TPD Lawyers Sydney — No Win No Fee TPD claims for NSW residents. Call 1800 318 002 for a free consultation.

Personal Injury Lawyers Cabramatta — No Win No Fee personal injury claims. Call 1800 318 002.

Learn more about No Win No Fee lawyers in Sydney — how it works, what it costs and what to expect from your claim.